January 2023

Reference rates serve as a market standard basis for calculating interest rates in various financial transactions and are thus also an essential component in trade finance agreements. The benchmark interest rates are calculated daily for various currencies and tenors. For Euro-denominated transactions, the EURIBOR (Euro Interbank Offered Rate) is considered the most important benchmark interest rate. It is published for five different tenors (1 week, 1 month, 3 months, 6 months, 12 months). In addition to the EURIBOR, other important reference rate benchmarks are the term SOFR (Secured Overnight Financing Rate) and the term SONIA (Sterling Overnight Index Average), and other interest rates used in interbank trading. Since the normalization of the interest rate environment in 2022, reference rates predominantly represent the highest proportion of total financing costs.

The tenors in factoring transactions depend on the underlying invoices and the agreed payment terms between suppliers and buyers, which mostly fall within ranges outside the published benchmark tenors for reference rates. As part of fair pricing, the reference rate should be adjusted to the financing term by linear interpolation. This type of fair pricing is often not considered in factoring agreements. Instead, the 3-month EURIBOR is typically used for reasons of simplification. This is a clear disadvantage especially in the current market environment.

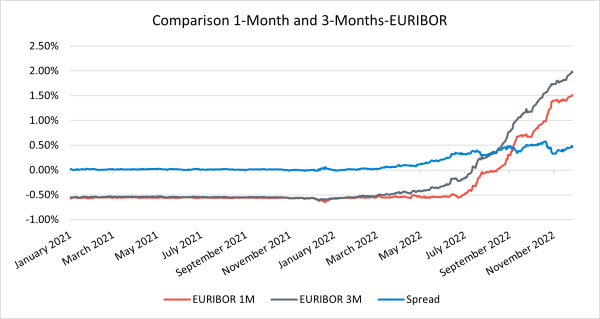

In times of rising interest rates, the importance of approximating the reference rate as closely as possible to the financing term becomes apparent. The following chart shows the development of the 1-month and 3-month EURIBOR in the period from January 2021 to November 2022:

In July 2022, the European Central Bank (ECB) ended the period of negative interest rates with its first key interest rate increase in six years. These were de facto not considered on the CRX Marketplace, as the reference rate used was floored at "0%". With the increase in key interest rates, EURIBOR also showed a positive development for the first time in years. The blue line shows the difference between the 3-month and 1-month EURIBOR. In a normalizing interest rate environment, this difference is up to 0.5% and higher.

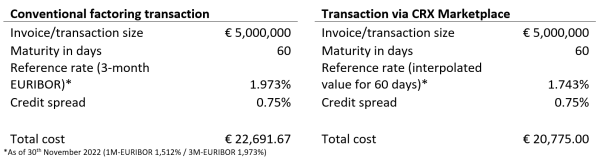

The following calculation compares the total costs of a conventional factoring agreement with the costs of the transaction on the CRX Marketplace:

The resulting cost savings show the economic advantage of a day-accurate reference rate interpolation. Especially in the revolving sale of receivables and in the sale of large volumes, the savings from this fair pricing make a significant difference in the overall expense. This underscores the importance of comparing all price components of a receivables transaction, including the cost of trade credit insurance or factoring fee.

Have we caught your attention?

Talk to our sales team. We’d be happy to show you in a demo what CRX Markets can do for your company.