July 2022

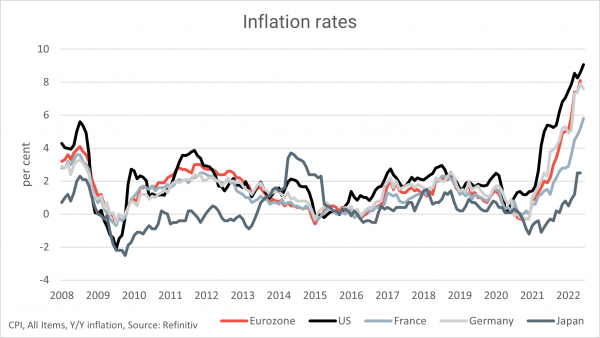

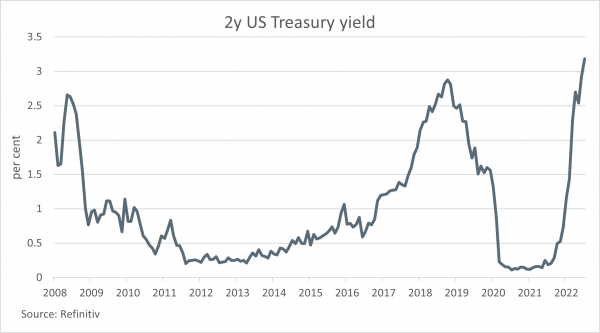

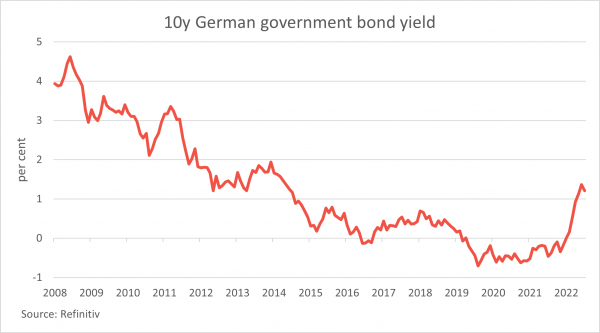

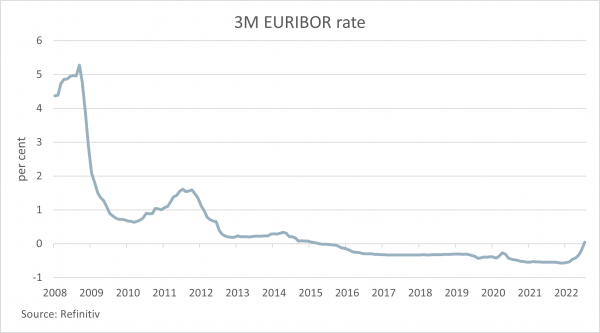

The world is in turmoil: continuing massive supply chain disruptions due to COVID-19, a military escalation in Europe that was unthinkable just 6 months ago and 1970s style price increases. All this happening simultaneously resulted in a polycrisis that caused shockwaves in the financial markets not seen since the global financial crisis. When inflation figures started to come in between 5 and 10% in developed markets, the world’s leading central banks were backed into a corner with no other option left than hiking their respective target or policy rates, thereby bringing the decade-old era of ultra-loose monetary policy to an end. The reaction in interest rate markets – and hence financing conditions for the real economy – followed immediately. 2y US Treasury yields reached 3.4% on 14th of June 2022, the highest level since the subprime mortgage crisis in 2007/2008. 10y German government bonds peaked at 1.37%, a 149 bps increase since its bottom beginning of the year. On the 14th of July 2022, the 3-month EURIBOR (a very common base rate in a wide range of financing agreements relied upon by corporates) was non-negative for the first time since August 2015.

Rising interest rates are responsible for various knock-on effects. Public and private market valuations dropped as (potential) future cashflows are discounted with higher factors and rising refinancing costs are a drag on future earning potentials. Borrowers, in particular high-risk borrowers, find it harder to access liquidity with banks and institutional investors becoming more prudent in anticipation of rising default rates. However, these are not entirely unwanted consequence as a cooling economy results in less demand and hence lowers inflationary pressure.

What are the consequences for Supply Chain Finance (SCF)?

From a macro perspective, stressed supply chains and rising borrowing costs for lower rated or smaller companies are a clear motivation for the larger constituents in global value chain to seriously consider SCF as a tool for supply chain stability. While 6 months ago credit and liquidity were abundant, this is clearly no longer the case. But what does this imply for existing SCF programs? An interesting technical detail that might see more attention over the following months is the use of reference rates in SCF agreements. The vast majority of SCF agreements (for both payable and receivables) use a bifurcated pricing mechanism where a credit margin (that compensates a bank for credit losses and the provision of equity/RWA) is added on top of a so-called reference rate (which is supposed to reflect the typically refinancing cost of a bank, i.e. the provision of liquidity). While the former is usually negotiated between a bank and the client, the latter is usually taken as a given market-standard. Why is this interesting? Such reference rates are typically “floored” at zero, i.e. whenever the reference is smaller than zero, it is assumed to be zero. This was extremely relevant over the last ten years and is no longer so since mid-2022. For banks, this typically implied an additional income as their refinancing cost were not floored at zero. Given that margins were negotiated, often in situations with price competition, banks started to compensate their margins with the windfall profit from flooring the reference rate. With this benefit now disappeared, many banks will be forced to enter into margin renegotiations with their clients. And usually, they have the possibility to do so as SCF agreements are typically not committed with respect to the pricing (or credit line).

At CRX Markets, we are convinced that a well-structured marketplace mechanism is ideally suited for discovering the fair and optimal price in such periods of fundamental repricing.